(LifeSiteNews) — Journalist James Corbett offered an in-depth analysis of Central Banking Digital Currencies (CBDCs) and stressed that citizens need to better understand CBDCs in order to know what’s coming.

Corbett said in his video titled CBDCs: Beyond the Basics (see video above) that “we have largely had all of this information occluded by the banksters [portmanteau of banker and gangster] in whose interest it certainly is to keep us in ignorance of how the banking system works […]”

The Basics of CBDCs

Corbett summarizes the basics about CBDCs that everyone should know before investigating further.

He offers the following bullet points as a summary:

- CBDCs are coming

- CBDCs offer central bankers unprecedented control over the economy

- CBDCs will be used to control society

In addition, Corbett notes that it is important to know that CBDCs are a “digital version of money a bit like a banknote” and that they “would be issued directly by a central bank.”

In the U.S. that would mean a CBDC would be issued by the Federal Reserve (Fed), in the EU it would be the European Central Bank (ECB) and in the U.K. the Bank of England.

RELATED: Examining the sinister growth of digital currencies around the world

Sign the petition to let Abp. Broglio know that you support his stance against the woke mob!

In a thrilling win against the leftist infiltrators in the Church, the U.S. Conference of Catholic Bishops (USCCB) made a key electoral decision at their Fall General Assembly in Baltimore, Maryland last week.

As reported on LifeSiteNews, Archbishop Timothy Broglio of the Archdiocese for the Military Services, USA, was elected Tuesday to serve as the next president of the USCCB.

Broglio has consistently defended Catholic teaching – his orthodox record has been a constant source of frustration to liberal bishops across the country. The military archbishop is one of a small number of prelates who:

- Opposed COVID-era restrictions on public Masses.

- Denounced COVID shot mandates for US Catholic servicemen.

- Supports freedom of conscience exemptions to jab mandates.

- Backed former President Donald Trump’s ban on gender-confused troops.

- Implemented guidelines prohibiting military chaplains from blessing same-sex unions.

- Recognizes homosexuality as a root cause of the clerical sex abuse crisis.

- Stressed that Pope Francis’ affirmation of same-sex unions is NOT Church teaching.

Abp. Broglio has shown support for our pro-life, pro-family, and pro-freedom movement – let’s show our support for him!

Say ‘THANK YOU’ to Abp. Broglio for standing up to left-wing bishops and defending Catholic values!

Tuesday’s election was a clear rejection of decidedly liberal candidates, including pro-LGBT Archbishop Paul Etienne of Seattle and radical leftist Archbishop Gustavo Garcia-Síller of San Antonio.

Left-wing Catholics are outraged about the results of the USCCB elections – now more than ever, Abp. Broglio needs the support of faithful Catholics like YOU!

STAND WITH ABP. BROGLIO against the woke mob and left-wing infiltrators of the Church! Add your name to the growing list NOW.

For more information:

Archbishop Broglio elected USCCB president

New USCCB head: Link between clergy sex abuse and homosexual priests ‘can’t be denied’

Corbett played a clip of Augustin Carstens, the General Manager of the Bank for International Settlements (BIS), that put many people who are worried about totalitarian control on alert.

“For example, in cash, we don’t know, for example, who’s using a $100 bill today,” Carstens stated. “We don’t know who is using a 1,000 pesos bill today. And the key difference with the CBDC is that the central bank will have absolute control on the rules and regulations that will determine the use of that expression of central bank liability. And also, we will have the technology to enforce that.”

Corbett stressed that is important to understand, however, that CBDCs are not a “singular, rigidly defined thing.”

“From the underlying technology used to issue, track and record these digital tokens to the network upon which they flow to the protocol that network follows, every part of central bank digital currency is customizable,” Corbett explained.

“There are some incredibly different ways that CBDCs could be implemented,” Corbett stated, adding that “if we are only looking for the one type of CBDC that everyone is, I think rightly, most afraid of” and a different version is introduced, we risk being called a “stupid conspiracy theorist” and getting fact-checked.

Therefore, Corbett stressed that it is paramount to understand CBDCs and the different forms that they may take. In order to do so, we have to understand the monetary system, specifically the Split circuit monetary system.

The Split Circuit Monetary System

Corbett plays a clip of activist filmmaker John Titus explaining the Split Circuit monetary system.

Titus explains that there are two circuits of money, the “Retail Circuit” and the “Wholesale Circuit,” also referred to as the “Private Circuit” and the “Public Circuit.”

In the “Private circuit” money is issued by Commercial banks (e.g. JPMorgan Chase), which are private entities. In the “Public Circuit” money is issued by Central banks (e.g. the Fed), which are officially public entities.

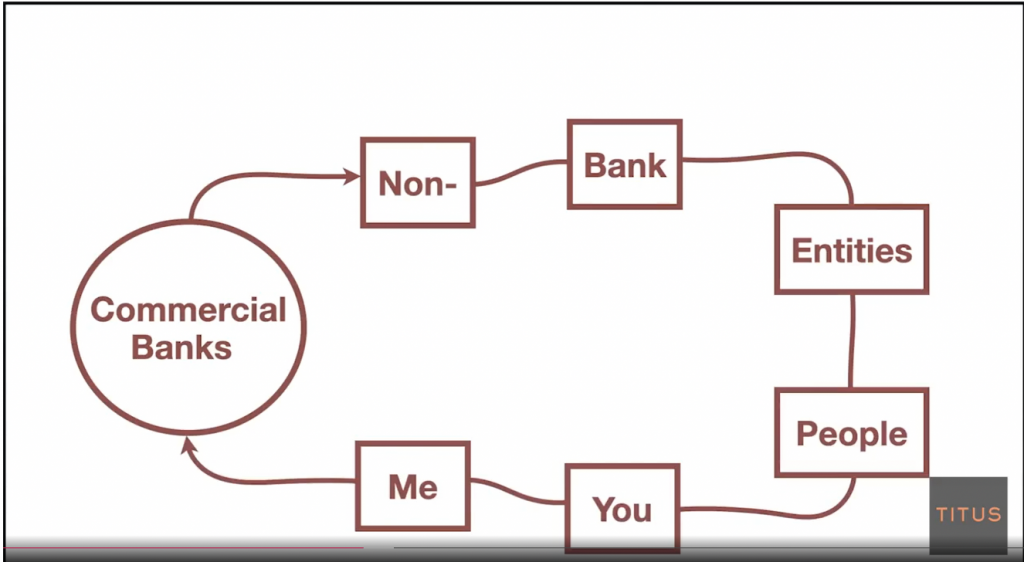

Titus illustrates the private or retail circuit like this:

Source: Screenshot Odysee video: https://odysee.com/@corbettreport:0/ep433-cbdcs:6

Commercial Banks issue money in the form of loans to Non-Bank-Entities (Businesses) and private citizens (“people like you and me”) who pay these loans back to the banks.

There are 4,357 banks issuing money through loans in America, according to Titus. “And that’s a bit much for the criminals, the totalitarians to control. They don’t like that,” Titus said.

In the public or wholesale circuit, the Central Banks (like the Fed) create money by printing cash or issuing loans to Commercial banks or countries (via government bonds).

“It creates money out of thin air, just like commercial banks do,” Titus stated.

Titus explained that there are three types of users in the Wholesale Circuit:

- Central Banks (Fed, ECB, etc.)

- Governments (e.g. U.S. government, especially the Treasury)

- Commercial Banks

The money in the retail circuit is sometimes called “Bank money” and in the wholesale circuits it is called “Reserves.” In both circuits, there are deposits of money.

The two circuits are separate from one another, as illustrated by Titus here:

Source: Screenshot Odysee video: https://odysee.com/@corbettreport:0/ep433-cbdcs:6

Titus explains that commercial banks have a “special place” because they are both issuers and users of money. Citizens and businesses (“you & me”) keep their deposits at commercial banks, who in turn keep their money at the Central Banks (e.g. the Fed).

Source: Screenshot Odysee video: https://odysee.com/@corbettreport:0/ep433-cbdcs:6

“But the Fed’s the totalitarians, they don’t like this system,” Titus said. “They want direct control. They’re going to get rid of the public/private distinction. They are going to change the two-tiered system and replace it with a central bank digital currency system […]”

In such a system, Commercial banks would no longer issue money and everyone would have their deposits directly at the Central banks and there would only be one circuit.

“And we’ll have one big happy totalitarian system,” Titus said while showing the illustration of a potential singular monetary circuit:

Source: Screenshot Odysee video: https://odysee.com/@corbettreport:0/ep433-cbdcs:6

Different Forms CBDCs could take

Titus explained the two circuits and showed the “worst case scenario,” that many critics of CBDCs are afraid of, namely that the retail circuit will be eliminated and everyone, including private citizens, will have their entire deposits directly at the central Banks in digital form.

However, this is not the only form CBDCs could take, and it may not be the likeliest one either, as Corbett explains.

Blockchain technology, for instance, the basis for digital currencies such as bitcoin, may not be the technology that central banks will use for their CBDCs.

“Blockchains that are actually used as blockchains may not even be actually effective tools of control,” Corbett said.

India’s version of CBDC, the digital rupee, may for instance not be on the blockchain, according to the statements by the Reserve bank of India.

Corbett cites an article from Business Insider which notes that “Blockchains are only one type of distributed ledger technology (DLT).” It is usually considered to be a “permissionless platform,” which means that anyone can participate and view all transactions that were ever made. Bitcoin, for instance, functions that way.

However, if a central bank wants to maintain total control over its CBDC and prevents others from viewing every transaction, a “permissioned system” is necessary, where only people with permission can access all the information about the CBDC.

“CBDC does not mean Blockchain, Blockchain does not mean CBDC,” Corbett concluded.

Corbett explains that CBDCs “comes in different flavors,” it could for instance be retail CBDCs or wholesale CBDCs (see explanation to Split Circuit Monetary System above).

This is illustrated by the example of the e-rupee, India’s planned version of the CBDC. According to a report by CBDC Insider, the Reserve Bank of India rolled out two separate pilot projects in November 2022, a retail digital rupee and a wholesale digital rupee.

These two programs could be separate, they could interact together or become one and the same thing eventually. It is not certain at the moment how exactly CBDCs will function in India or elsewhere in the world, as Corbett explained.

Corbett stressed that there are “lots and lots of different ways that this can be implemented,” and that people who are rightfully concerned about the “nightmare future of CDDCs, where the central bank will be able to directly control what you are purchasing, isn’t necessarily the way that they are going to implement it.”

The different players involved in the monetary system

Corbett explains why the central banks may not replace all other forms of payments with CBDCs, since that might destroy the whole monetary system and with it the source of their power and control. There are competing parties, including commercial banks and big tech companies, within the monetary system that may prevent total control of the money by the central banks.

An example of this is that the American Bankers Association (ABA) recently “raised numerous concerns about implementing a retail or intermediated CBDC that were not addressed by the New York Fed research.”

While the ABA welcomed a wholesale CBCD, since it “could deliver significantly faster cross-border transactions,” between central banks, they were concerned about a retail CBDC because it would represent an “’advantaged competitor’ to retail bank deposits, ultimately moving money away from banks and into accounts at the Fed where the funds cannot be lent back into the economy.”

Corbett explained that this shows that there are different interests among the bankers and it indicates that not all of them are on board with a retail CBDC.

Furthermore, there are big payment apps like the Chinese Alipay, which has over one billion users and handled 16 trillion dollars in payments in 2019. Alipay is a competitor to CBDCs as well, as people can load money into their Alipay wallets and pay with it using the Alipay app instead of a central bank currency like cash or CBDC. Alipay is even excepted as a payment method at Walgreens in the U.S., according to a report by The Economist.

PayPal is another example, similar to Alipay, where, if people keep their money inside the system, PayPal can basically fulfill the function of a bank without being a bank.

Meanwhile, Facebook and Amazon are also developing their own version of digital currencies that could act as competitors to the central banks and severely limit their control over the economy.

This shows that central banks, retail banks, and big tech providers are in fact competing over the payment systems, so there is hope that it is not going to be “just one monolithic control structure in which everybody is working towards the same vision and agenda for the same purposes,” Corbett states.

Another sign that CBDCs may not take over the entire monetary system is the latest statement by Fabio Panetta, Executive Board Member of the ECB, during the Digital Euro conference.

Panetta said that the ECB is considering to restrict the amount of money someone could hold in their digital Euro wallet, e.g. to € 3,000, because they don’t want to risk that people move “their deposits out of their banks or their money out of financial intermediaries.”

“And this, especially in crisis periods, could cause financial instability, and we don’t want to do this,” Panetta stated.

Corbett said that the reason why central banks may not want to control 100% of the market share with CBDCs is that “they understand that if they start tinkering with this, they might collapse the commercial banking sector as it exists and completely destabilize banking as we know it.”

“So, the more power and control the central bankers control for themselves and bring in for themselves, the more they destabilize the entire financial system as they’ve set it up, which may not be something that they’re looking to do,” Corbett stated.

In summary: 3 fallacies (PSYOPS) to avoid

To sum up the information about CBDCs, Corbett offers three fallacies or PSYOPs that we should avoid:

- The “Bitcoin PSYOP:” Bitcoin, Blockchain, digital currencies, and CBDCs are all the same.

- The “CBDC PSYOP:” CBDC can only be implemented in one way, with only one technology, to ensure total control for central banks.

- The “bankster PSYOP”: the bankers are all from the same class, a monolithic organization, have the exact same interests, and are all working for the exact same agenda.

As was shown in this article, the situations with CBDCs and the monetary and banking system are more nuanced and complex than these PSYOPs would suggest.

Corbett said that the “common thread between those various PSYOPs is that it’s always about dumbing down the conversation to a level where essentially it doesn’t really matter what your opinion is on these subjects because it’s so ill-informed that you do not understand what it is that that’s really happening, and you never will until the change happens and you’re just swept along by it.”

Solutions

To know what’s coming, and to avoid being “swept away” by the changes, as Corbett puts it, we have to first understand what CBDCs are on a deeper level and stay up-to-date with the developments of the central banks, especially in the country we live in.

Another possible solution is to make sure you have alternative “survival currencies,” in case a total control state through Digital IDs, biometric surveillance, CBDCs, and social credit scores are implemented and you are cut off from the monetary system.

READ: Tyranny looms as digital IDs and currencies roll out around the world

Corbett presents his recommendation for survival currencies, including precious metals, cryptocurrencies, barter deals, and others in this video.